Abha Thorat- Shah

Executive Director, Social Finance - British Asian Trust

Using the Right Capital for the Right Job

The British Asian Trust was founded in 2007, by His Majesty King Charles III and a group of British Asian business leaders, to tackle widespread poverty, inequality and injustice in South Asia. We are global pioneers in social finance, with a strong track record of driving successful collaborations and applying social finance approaches to solve social and economic challenges in South Asia. We work to address challenges and barriers faced by non-profits, governments, CSR donors, foundations and other key stakeholders with social finance tools like impact bonds. So far, we have launched the world's largest education and skilling development impact bonds in India, mobilizing around $25mn of capital to improve the lives of 250,000 people.

Q1. What can you tell us about your approach using blended finance, and how it has evolved over the years?

The real driver for us getting into the blended finance space was to explore critical answers to the questions we had around the impact of existing development approaches: could we achieve bigger and better impact if financing of development projects was approached differently? What needs to change and how do we do it? Could we try new approaches and leverage new sources of finance to do this? Which types of social problems are better suited to this approach?

The need to think differently about funding, outcomes, and programme effectiveness was the starting point for us. And having asked ourselves the above questions, we made the decision to expand our work to embrace blended finance as it strongly aligned with our values as innovators and disruptors.

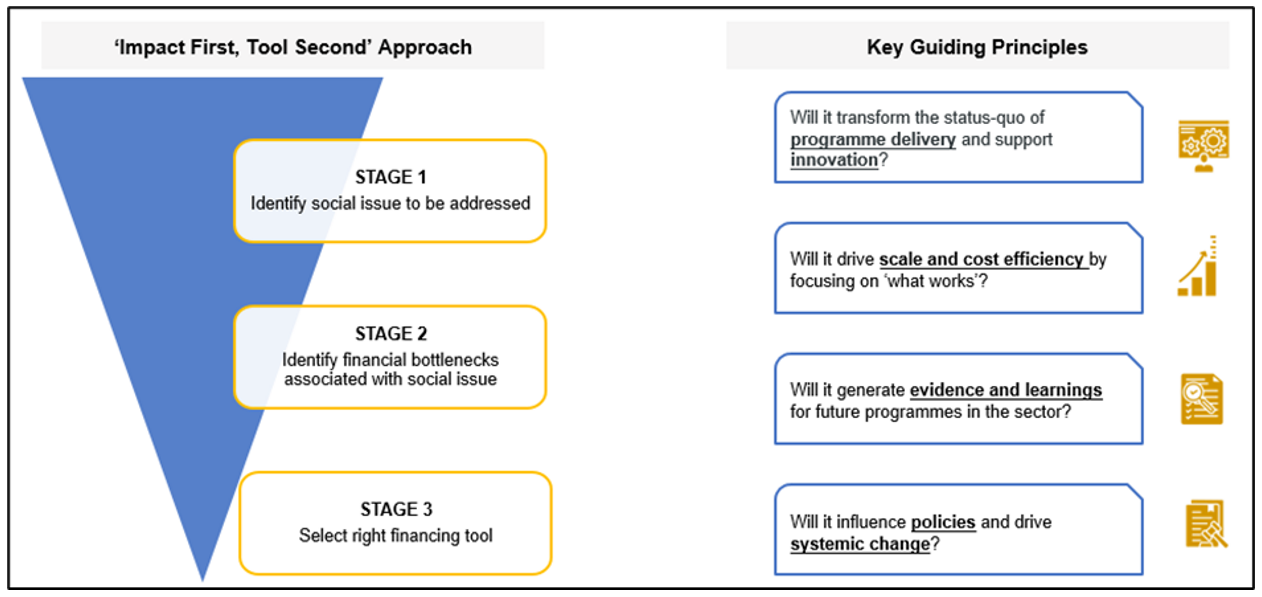

Over the last five years, we have adopted an 'impact first, tool second' approach to design our programmes. As shown below, we start with the social problem or challenge to be addressed, identify the bottlenecks and key impact levers associated with the issue, and then design the right blended finance instrument to address the bottlenecks and trigger the levers.

We do not believe in a 'one-size-fits-all' approach - we are not looking around to identify where to do the next development impact bond (DIB). We want to identify if a blended finance tool can challenge the status quo of the problem in focus. Will it support innovation? Will it support scale? Will it drive cost efficiencies? Can we generate learnings or evidence for a new way of doing things? Will it help inform policy or good practice in the sector? What is the additionality of blending capital to resolve the social challenge?

Q2. Can you describe blended finance transactions or products that the British Asian Trust has been involved in?

At the British Asian Trust, we have led and co-developed the following transactions in blended finance:

In the field of education:

- We initiated our work in blended finance with the Quality Education India DIB (QEI DIB), that aimed to drive a deep focus on learning outcomes, support diverse education models, put evaluations at the heart of the project and enable robust use of data to make decisions. The QEI DIB ran from 2018 to 2022, through the peak of the pandemic, and really showed how the focus on innovation and outcomes enabled organizations to continue to deliver results in the face of massive challenges.

- In August 2021, we launched the Bharat Edtech Initiative in collaboration with Michael & Susan Dell Foundation, Sattva Consulting and GiveIndia to enable increased EdTech access and engagement for children from low-income communities. The fund also aims to drive evidence and learning on 'what' works in edtech to enable increased learning outcomes. We work on the Steering Committee of this programme and drive key programmatic decisions on linkages to learning outcomes.

- We are now building on learnings from both these programmes to a new fund which is currently under development - the Back-to-School Outcomes Fund. As part of this fund, we are looking to drive a deep focus on the goals enshrined in the NIPUN Bharat Mission on Foundation Literacy and Numeracy (FLN) for all children in India.

We have also taken a similar approach to the skilling ecosystem. In October 2021, we launched the first-of-its-kind Skill Impact Bond in partnership with National Skill Development Corporation, Michael & Susan Dell Foundation, the Children's Investment Fund Foundation, HBSC India, JSW Foundation and Dubai Cares, with FCDO (UK Government) & USAID as technical partners. The coalition has brought together a US$14.4 million fund to benefit 50,000 young people in India over four years. The target group includes 60 percent women and girls and to equip them with skills and vocational training and provide access to wage-employment in Covid-19 recovery sectors including retail, apparel, healthcare, and logistics.

Q3. The British Asian Trust has been a pioneer of various blended finance transactions and structures in the education sector, much like the Quality education India DIB and the ecosystem driven Bharat EdTech initiative. What are the emerging lessons and challenges that you see needing greater attention by investors as well as policy makers in the education sector?

Our goal with programmes like the QEI DIB and Bharat EdTech Initiative was to drive better learning outcomes, diversify funding for big social challenges development and ensure value for money. The key learnings derived from these programmes are:

- Learning #1: The QEI DIB demonstrates a strong case to link funding and incentives to concrete improvement in learnings outcomes rather than only to inputs or activities. The final results of the programme showed that QEI DIB students learned 2.5 times more than students in non-participating schools. Additionally, twice as many students achieved age-appropriate learning levels compared to non-participating schools.

-

Learning #2: The selection of intervention models should be based on learning contexts and investment objectives. For instance:

1. Given the high learning impact, direct models can be effective where students lag more or rapid gains are the objectives, however, scaling these models might require high annual investments.

2. Indirect models are well suited and cost effective where large scale change or systems transformation is the goal. - Learning #3: EdTech, particularly personalized adaptive learning (PAL), is a promising model where large variations in learning levels exist and students require customized support. As demonstrated by the Bharat EdTech Initiative project, three critical elements need to work together for successful adoption of EdTech - i.) high quality, Bharat-ready EdTech products (low-tech and asynchronous were more suitable) ii.) enabling environment at home and in community and iii.) dedicated on-ground support and learning routines.

- Learning #4: Flexible funding allows implementation partners to adapt their interventions and navigate on-ground challenges to focus on outcomes e.g., QEI DIB implementation partners pivoted their models during the Covid-19 pandemic. In addition, adaptability on part of investors, funders and technical partners is crucial in ensuring success of the programme.

- Learning #5: Our Cost Effectiveness Study on Education Interventions highlights that high quality interventions can deliver one additional year of learning per student in existing government school settings for an additional investment of INR 1000-3000 per student. This can serve as a useful benchmark while procuring interventions.

- Learning #6: The key challenges are around simplifying and standardizing assessment mechanisms in the education sector to help build evidence to improve efficiency and decision making at the policy level.

Q4. What according to you are some of the best practices that you can share from your experience, to measure impact through blended finance activities?

We can speak best to best practice in the results-based financing space but some of our learnings can be applied more widely to the blended finance sector:

- Ensure that key capital providers such as social investors, grant makers, government are all aligned on the shared impact goals of the project, their definitions, indicators and measurement and their role and use of capital in pursuit of these impact goals

- Ensure that you include key indicators on financial returns, sustainability and cost efficiency, alongside impact indicators

- Invest in striking the right balance in evaluation methodologies - those that are rigorous, objective and robust, but can work concurrently with project implementation and can be agile and flexible

- Ensure that the right capital is used for the right job

- Share the learnings, data and results widely with the sector as a public good so that the evidence/data can be used to design future projects

- When working with nascent sectors, ensure that you build capacity of partners and provide technical assistance to collect, manage and use data for decision making

Q5.Based on your experience in blended finance to date, what gaps and opportunities do you see in the blended finance market?

India has seen a strong growth in blended finance approaches with a broad range of tools being applied in more sectors. According to the India Impact Investing Handbook, the total impact capital deployed from 2019 to 2021 was estimated at $14.44 Bn including 1048 deals.

Key areas that need further attention include:

- Need for more players who can deliver the key enabling factors for success that can be used as the basis for decision-making i.e., design, performance management, evaluation etc.

- Need for clarity on legal frameworks, standardized templates and simplified contracting.

- Need for some of the learnings and principles that drive success in this work to be shared more broadly with the sector - learnings can also be applied to mainstream funding including Government procurement.

- Need for new funders and diversified sources of funds to come in and addressing entry barriers for new actors.

Q6. What can the blended finance and impact ecosystem do better to engage and receive funding support from India's CSR and philanthropic investor community?

CSR and family/individual philanthropy are two sources of domestic impact or development capital that can be truly catalytic. According to Bain's India philanthropy Report 2022, both CSR and family/HNI giving are poised to grow at a robust rate in the coming years, driven by increasing wealth and a rise in the number of technology entrepreneurs. To tap into the potential of CSR and philanthropic communities, the blended finance ecosystem needs to focus on three key aspects:

- Open dialogues: We need to engage in open, honest and evidence-backed conversations around not only the benefits of blended finance, but also the challenges (design, regulatory, operational, legal etc.) and proactively try to solve those challenges. Simple, concise and jargon-less communication that demystifies the principles of blended finance and makes them less abstract and more real will allows more voices to be heard. Champions and peers from within the CSR and philanthropy sectors can help in developing a more empathetic understanding.

- Fit-for-purpose products: We need to listen to these stakeholders, understand their intent and pain points and design fit-for-purpose tools that can work within the Indian context, deliver impact and simultaneously also achieve specific objectives that donors may have (scale, leverage, choice of geographies, visibility, attribution, CSR or ESG compliance etc.)

- Partners, not funders: This approach works both ways. The blended finance ecosystem needs to create opportunities for CSR and philanthropists to come in as thought and design partners and not just funders or buyers of impact, whereas donors need to cultivate enabling internal systems and processes that allow them to partake as core partners, demonstrating commitment, trust, flexibility and ownership.

Q7. Developing countries have a lot of work to do to recover from the pandemic and need to better position themselves to weather the next global shock. Governments need to take a long-term view, which means investing limited public funds to catalyze private investment. What role do you see the Indian government and regulators playing in supporting the blended finance ecosystem?

Let us first acknowledge the role that the Indian regulatory environment has already played in building the blended finance ecosystem. Compared to many other developing countries, India has relatively mature financial, legal and regulatory systems and processes that offer clarity, definition, consistency, safeguard investors and drive confidence. Indian government and regulators have been ahead of the curve in aspects such as mandatory CSR, approving social stock exchanges, mandating ESG disclosures. They have demonstrated a healthy track record of innovative structures such as alternate investment funds, social venture funds, credit guarantees, micro insurance etc. This fundamentally sound and stable architecture has been one of the key drivers of blended finance in India.

To further boost and accelerate the growth of this sector, the regulators could focus on three specific aspects - continuing to evolve CSR regulations to allow companies to participate in blended finance, creating and/or evangelizing fund structures that allow mingling of different types of impact capital and continuing to emphasize on transparent and standardized reporting requirements and disclosures on impact capital. With respect to the latter points, we are very excited to explore the potential of the social stock exchanges, recently notified by the regulators, in accelerating blended finance through enabling better discovery of social organizations, standardized reporting norms and emphasis on social audits, all of which can reduce transaction costs and build transparency and credibility in blended finance. We are also keen to work with various government and semi government bodies and policy makers to mainstream some of the principles and learnings from our work on outcome-based financing in India and globally.