Vineet Sukumar

Founder and CEO,

Vivriti Asset Management

Vivriti Asset Management

White Space in Mid-market Credit Segment for Blended Finance

Vivriti Group specialises in the mid-market performing credit space, a segment which presents a large white space and remains untapped by both local and global capital. Our responses to the questions below are related to the mid-market performing credit space and not other asset classes where other applications of blended finance structures are possible.

Q1. The blended finance ecosystem in India has witnessed sustained through gradual growth, and is now at a tipping point, poised for accelerated adoption. As the pandemic creates pressure on overall developmental resources, what are your views on the relevance and scale of blended finance transactions in India?

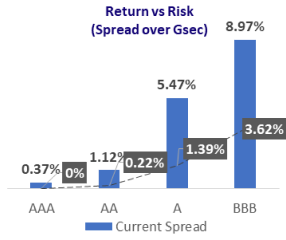

Indian debt capital markets are shallow and are skewed towards larger and higher rated enterprises. As per Vivriti estimates, the mid-market segment comprises of more than 22,000 companies which carry an investment grade rating but are overly reliant on bank financing as the access to capital markets remains low. This space has historically seen very low default rates and the current spreads over risk free more than compensates for the incremental risk. However, most investors perceive this segment to be risky, a conclusion which is not supported by the actual underlying data.

The space is covered with established companies with proven business models, the majority of which have a positive EBITDA

while Spreads in the 'A' and 'BBB' rated entities are relatively higher than AAA / AA peers without a commensurate increase in credit risk

As can be seen from the above data, large amount of capital which is currently invested in AAA/AA rated companies can be unlocked for A/BBB rated companies with the use of blended finance structures. Hence, blended finance can play a big role in deepening the debt capital markets in India and is a highly scalable proposition.

Q2. Can you describe blended finance transactions or products that your organization has been involved in? What can you tell us about your approach using blended finance, and how it has evolved over the years?

Vivriti Group has been at the forefront of Blended Finance initiatives in India. Given below are some of the notable blended finance transactions where Vivriti Group played a pivotal role.

-

US$50Mn Loan Guaranty Program with USAID, and DFC for women empowerment

The United States Agency for International Development (USAID) and the U.S. International Development Finance Corporation (DFC) have jointly sponsored a US$50 million loan portfolio guarantee to Kotak Mahindra Bank (KMBL) to support increased access to finance for women borrowers, and micro, small and medium enterprises (MSMEs) across India. The program is supported by Vivriti Capital (Holding Company of Vivriti Group), which will provide a US $1 million first loss guarantee. -

Vivriti Capital is a partner financial institution for ADB's Risk Participation and Guarantee Program for supporting micro entrepreneurs.

ADB's Risk Participation and Guarantee Program is a credit enhancement and a risk-allocation tool, designed to address a market gap and promote local currency lending to micro-finance institutions. ADB partners with micro-finance institutions, to increase their access to local currency funding and address the financial needs of millions of people, at the base of the pyramid across the region. Given its risk-sharing structure, the program encourages private sector participation on market-determined terms. Vivriti Capital has relied on this program to direct funding to smaller MFIs who have limited access to capital markets. - Vivriti Samarth Bond Fund

Vivriti Samarth Bond Fund (VSBF) is a US$35Mn blended finance vehicle to provide liquidity support to enterprises during COVID-19. The fund invests in lower rated (A/BBB) retail financial services NBFCs which lack access to capital markets. The fund is divided into two tranches. The senior tranche comprises 80% of fund size and the junior tranche comprises 20% of fund size. The senior tranche has a priority in payment of cashflows and has been rated CRISIL AA+(SO) for capital protection.Philanthropic investors like The Michael and Susan Dell Foundation have provided catalytic capital in the junior tranche. This has allowed institutional investors like Banks, Insurance companies and corporates to participate in the highly rated senior tranche. These investors would find it difficult to directly invest in A/BBB rated entities. Thus, by employing blended finance VSBF has been able to direct commercial capital to impact related investments and helped create a capital market footprint for lower rated issuers.

-

Vivriti Group's approach to using blended finance

As discussed in the earlier question, within the mid-market performing credit space there is a significant mismatch between the perceived and actual risk of the lower rated entities. Vivriti Group's approach has always been to solve for this dichotomy using market-based structures. Vivriti has aimed to solve for this using a combination of:-

guarantee-based structure where Vivriti Group provided the first loss support with the larger second loss guarantee coming from DFIs, and capital being provided by Banks.

- fund structures that bring in participants in senior and subordinated tranches, with impact capital playing a role in the subordinated tranches This structure allows a large variety of investors from DFIs to commercial investors and HNIs to participate in the impact-oriented financing.

Over time, the fund structure has been proven to be more scalable. By shifting from a bilateral structure like a loan to capital market instruments like bonds/debentures we are helping to create a capital market footprint for smaller issuers which will over time help them to directly tap into larger investor base of capital market investors.

Q3. Given your wide experience, what are the emerging / priority areas or sectors (like healthcare, climate action) which you anticipate will attract greater investor attention in the next five years?

India has a large credit gap in many of the key priority sectors. Some of the sectors which are likely to attract greater investor attention include:

- Healthcare: Setting up hospital and diagnostic services in Tier2 and Tier-3 cities. Indigenous production of low-cost medical devices.

- Clean Energy: Distributed projects in open access and commercial and industrial space.

- Agriculture: Post harvest infrastructure to reduce losses caused by supply chain inefficiencies.

- Infrastructure: Warehousing, digital infrastructure, and logistics.

- Financial inclusion.

Q4. With Vivriti Samarth Bond Fund, you have created an alternate investment fund (AIF) structure which utilizes a tiered blended finance structure with subordinate philanthropic funding from impact foundations and HNIs. What are some of the key learnings on how the blended finance ecosystem can engage and receive greater funding support from India's CSR and philanthropic investor community?

As per the current regulations, investment in a blended finance structure like Vivriti Samarth Bond Fund (VSBF) does not fall under the ambit of CSR or philanthropic activities. This gets classified as an investment activity. However, this should not prevent corporates from participating in initiatives like VSBF.

In general, there is a misconception that impact investments earn below market returns and require DFIs and philanthropic investors to provide concessional capital. However, structures like VSBF do not require concessional funding, unlike some of the other blended finance structures. Investors can expect to earn commercial returns which are commensurate with the risk of the class they are investing in. Thus, by investing in blended finance structures like VSBF India's CSR and philanthropic investor community can look to combine purpose with profit and earn risk adjusted returns by investing for impact.

Q5. There is a greater need for capacity building and collaboration in the blended finance ecosystem given the multiple stakeholders in each transaction. Can you give an example of a transaction highlighting the following - What unique capabilities and expertise did each participant bring to the table? How were participants brought together?

The Vivriti Samarth Bond Fund transaction brought together multiple stakeholders with a varied set of preferences. We had commercial investors like Banks, Insurance Companies, Corporates, Family Offices and HNIs in the senior tranche who provided long-term patient capital. We had philanthropic investors like the Michael and Susan Dell Foundation (MSDF) who provided catalytic capital in the junior tranche which acted as an important signalling mechanism for the senior tranche investors. MSDF also brought in its expertise on impact management which helped to strengthen the impact measurement and tracking at the fund level. Participants were brought together by Vivriti Asset Management (VAM) which plays an important role in identifying and allocating capital to impact oriented enterprises and managing the whole transaction end to end. VAM also maintains a skin in the game by investing significant amount of its own capital in the junior tranche. Using a fund structure makes it possible for investors with varied preferences to co-exist in the same structure.

Q6. What lessons can you share with other investors and asset managers, that may be operating at a smaller scale, on how to consider different blended finance instruments?

Choose instruments and structures which are market oriented and scalable. Try to find a market solution so that the instruments/structure can be self-sustaining without the need for a concessional capital. As long as, the structure is scalable it is okay to start small to establish a proof of concept. Once the concept is proven, it becomes easier to scale subsequent structures. While VAM began with a US$ 35 mn corpus at VSBF, VAM could quickly scale up the concept with larger pools of capital. VAM presently operates seven funds today, where corpuses have increased with time and with more investors coming on board.

Q7. Based on your experience in blended finance to date, what gaps and opportunities do you see in the blended finance market?

There is a lack of awareness about blended finance and how it can be used in the context of impact investments. Also, there is a lack of literature and case studies of historic blended finance transactions which have taken place in India. There is a need to educate the regulators including the securities market regulator, central banks and others on the need and use cases of blended finance.

The Government will need to provide specific incentives to enable scalability of blended finance. Further, regulators should incentivise and remove roadblocks in the way of financial markets to increase allocation to blended finance structures. Some areas of intervention could be:

- Priority sector classification for banks

- Reducing risk weights for banks to invest into blended finance AIFs

- Increase limits for insurance investors to invest into blended finance AIFs

- Specific inclusion into CSR

- Specific tax breaks on investment income

The gaps highlighted earlier are also the areas of opportunities. With growing awareness and availability of data we can expect to see an increasing adoption of blended finance which will help to expand the market for impact investments.