Priya Naik

Founder & CEO, Samhita Social Ventures

Blended Finance: A Blueprint to Collaborate

Samhita Social Ventures works to address the most challenging socio-economic problems in India by leverage their strengths, experience, and knowledgs to fulfill their vision. They work with multiple stakeholders to curate strategies, design solutions, and forge strategic partnerships that have the potential to create impact at scale.

Q1. The blended finance ecosystem in India has witnessed sustained through gradual growth, and is now at a tipping point, poised for accelerated adoption. As the pandemic creates pressure on overall developmental resources, what are your views on the relevance of blended finance transactions in India?

Even before the pandemic, it was estimated that more than USD 500 billion of private capital was needed to achieve India's sustainable development goals by 2030. One of the consequences of COVID-19 was the capital departure from other cause areas, casting doubt on funding critical development projects in the years to come. Traditional methods of funding alone are not going to be enough for India to achieve its SDG goals; blended finance is the support we can lean on to bring together multiple stakeholders - public, private and philanthropic - to help finance development outcomes.

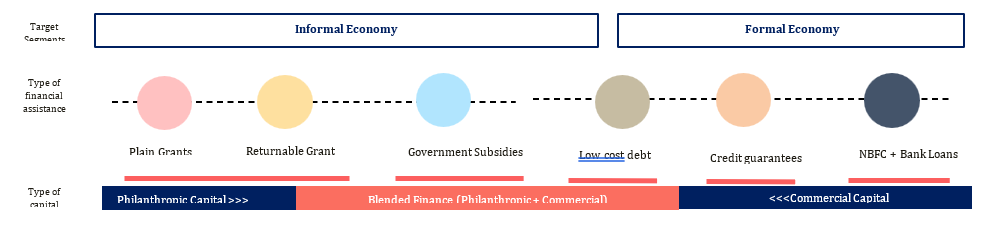

Blended Finance in India is not a new concept. We've seen blended finance structures used in India across sectors such as in education we have - The 'Educate Girls' Development Impact Bond and British Asian Trust's Quality Education India Development Impact Bond; in livelihood we have BAT's Skill Impact Bond and Samhita's Returnable Grant; and in healthcare we have Utkrisht Development Impact bond, NITI Aayog and Samridh Healthcare Blended Finance Facility

However, there has been limited visibility of the success that such instruments have been able to deliver as well as limited clarity and hesitancy from a CSR compliance lens.

Q2. Given your wide experience, what are the emerging/priority blended finance areas or sectors (like livelihoods, climate action) that you anticipate will attract greater investor/donor attention in the next five years?

We see areas such as climate action, green infrastructure, microentrepreneurs and gender empowerment that will benefit from different blended finance instruments. s, and we can already see many players set up large collaborations to address these needs. The role that blended finance can play here is pivotal. A blended finance approach can give us the blueprint to collaborate, help lower risks and transaction costs, as well as expedite deal flows.

To deliver maximum impact, the instrument needs to be significantly customized for each cohort group, and in areas of financial inclusion and livelihood we are pairing the blended finance instruments such as the returnable grant with financial literacy interventions to provide access to formal capital. This will nudge the communities toward wealth creation behaviours and set them on a pathway to prosperity.

Q3. Can you describe blended finance transactions or products that Samhita has been involved in? What can you tell us about your approach using blended finance, and how it has evolved over the years?

As a response to the COVID-19 pandemic, we created and designed the Returnable Grant - an innovative blended-finance instrument that provides short-term, affordable and flexible capital (zero interest and zero collateral) to individuals and entrepreneurs, with a moral - and not a legal - obligation to repay. Co-designed with the Michael and Susan Dell Foundation, this structure has enabled some of the most vulnerable communities that were affected during the COVID-19 pandemic to access credit when they needed it the most and payback at a time and manner that did not compromise their financial situation. Participants across all cohorts demonstrated repayment rates in the range of 97%

Returnable grants allow money to be directly credited into the participants' accounts or given out as cash equivalents such as vouchers. This process is supported by nonprofits organisations or non-banking financial company (NBFC) partners. Once a returnable grant is repaid, it is circulated back into the repayment ecosystem to support additional participants with similar needs. This design allows RG to benefit 5-7x the number of individuals when compared to a simple grant over multiple years, therefore, making it a potentially catalytic tool to propel economic recovery for individuals.

Through a 'graduation' model, along the blended finance continuum, focusing on the following types of participant profile, we aim to integrate them into the formal economy

- First to income, first to credit: Individuals who have recently started earning but have not accessed credit

- First to credit: Individuals who have previously relied on the informal market for credit

- First to formal credit: Individuals who have previously taken informal credit loans, but are now in a position to access formal credit

The blended finance continuum combined with a financial literacy training and a pre-credit score allows us to match the right individual with the right tool that works for them. In addition, we are working to create a pre-credit score with financial institutions and experts, such that can be used by banks and NBFCs to offer credit to first time borrowers; acting as a proxy for credit ratings and proof of ability to payback. Beneficiaries develop a credit history due to the platform taking on the initial risk, which enables them to gain access to other financial services provided by the formal financial sector, and gain greater financial security.

Q4. Through the REVIVE Alliance, Samhita has participated in some unique blended finance structures. What are some of the key learnings? How can similar ecosystem-level initiatives be replicated in other sectors?

During the pandemic, the Returnable Grant was used to provide access to short-term credit for vulnerable communities, especially women, informal works and microentrepreneurs.

We saw a large percentage of the RG being been used towards, household expenditures, business inputs and expansion, dispelling concerns that direct cash transfers would be abused or misdirected into non-business consumption.Our working hypothesis was that repayment rates would be higher for cohorts working with partners with a strong community connect than with micro-finance initiatives, but our data so far indicates that repayment rates do not vary

In skilling, the RG model can be used as a catalytic finance solution to lend to the skilling ecosystem -for initial training fees and a loan model, zero interest EMI per month to repay training fees only after placement

With the aim to move recipients out of poverty, we used the RG to graduate individuals who repaid once they moved into income-generating activities. The Returnable Grant when given to first time borrowers, combined with critical interventions such as financial inclusion and generation of a pre-credit score (to objectively assess credit worthiness before an individual has accessed formal finance), can put individuals on a pathway to access formal credit from the formal banking system (saving facilities, credit and insurance mechanism and loan. This will help them avail loans from formal sources and increase their savings.

Key Insights that emerged throughthese engagements

- Flexible: can be used as a standalone instrument or layered on existing programs across sectors such as skilling, livelihood, healthcare, climate

- Catalytic: The Returnable grant puts a participant on a journey an accesscredit in a formal capacity and opening up other avenues and pathways that were previously not accessible.

- Plug and Play Model: Fit well into existing delivery systems, e.g. can be added to the skilling training form the lens of capital to pay for skilling programs that are more market relevant

- Build financial empowerment: The RG coupled with financial will help to raise the standard of living and contribute to overall growth.

Q5. What can the blended finance and impact ecosystem do better to engage and receive funding support from India's CSR and philanthropic investor community?

The private sector is not a homogenous group of potential funders, but a diverse group with different motivations and constraints when it comes to adopting blended finance instruments. We work with 4 types of funder archetypes:

- Anchor Funders: Ecosystem builders aligned to initiatives that demonstrate potential for impact at scale.

- Focused on Stakeholder Impact: Strategic focused on supporting individuals in their supply chain

- Innovators: Bring their expertise to support specific interventions or activities for a target group

- Impact-Led but Sector Agnostic: Impact maximizers that aligned to creating impact not tied to a cause or issue area

It is important for all stakeholders to have a clear understanding of which instruments are readily available, and how to incorporate them into financial structures to shift theinvestment risk-return profile to attain more favourable terms. While engaging with CSR and philanthropic community, it is critical to ensure that blended finance transactions are also aligned to their interests and demonstrates business opportunities. Moreover, it is critical to collect and disseminate best practices, learnings, impact on financial returns and playbooks.

Since the pandemic, more actors have been pursuing collaborative initiatives to mitigate risks and incentivize greater investment in sustainable development. Building on these collaborations can not only help lower risks and transaction costs, but even expedite deal flows.Strong governance frameworks around decision-making and reporting would help in providing comfort to donors.

Q6. What role do you see the Indian government and regulators playing in supporting the blended finance ecosystem?

Most of REVIVE's Intervention's are aligned to the Government of India's priority areas – be it providing social security access to all, accelerating digitisation via the Digital India Mission, financial inclusion through the Pradhan Mantri Jan Dhan Yojana, and entrepreneurship support to promote innovation in the country.

The government of India has already recognized the potential of blended finance and has shown its commitment through their announcement and promotion of thematic funds for blended finance in areas such as climate action, digital economy, pharma and agriculture. The Government of India has also committed a share of 20% with the funds being managed by private fund managers. This move is expected to spur further investment for CSR and private players to notice and adopt blended finance as a compliant and impactful tool. Moreover, the SAMRIDH Health Blended Finance Facility supported by Atal Innovation Mission (AIM) and NITI Aayog, is a reinforcement of their commitment in building a blended finance friendly eco-system.

If government and regulators are able to formally recognise and support initiatives such as the pre-credit score and social rating framework, this will allow for widespread integration and legitimacy

Q7. Based on your experience in blended finance to date, what gaps and opportunities do you see in the blended finance market?

Blended finance is not a homogenous one size fits all – there are many instruments and approaches, some more suited to certain sectors. The challenges or opportunities here is the need to leverage blended finance instrument according to the need of the relevant stakeholder, and design a structure that works.

Blended finance is really a solution to mobilise large scale capital; it de-risks potential investments, gives you access to increase investment, impact and opens up collaborative and partnerships. As a result, it can help you build up capability or, or work with existing capabilities. This is something that we saw when we implemented the Returnable Grant through an Alliance approach. The Returnable grant is designed to be compliant, quick to design, structure and deploy, as well as customise it to scale.

One of the challenges we have faced is that although it is discussed a lot, when we look at the mobilisation of blended finance activities that are unfolding, unfortunately adoption numbers have not gone up. Hence, what we need are more private sector companies and corporates that have adopted blended financial instruments to evangelise and speak about it and their experience.

We have to move the blended finance narrative to attract commercial finance, blending across a range of development contexts, sectors and SDGs, have a common framework and understanding and more evidence to showcase effectiveness of blended finance.