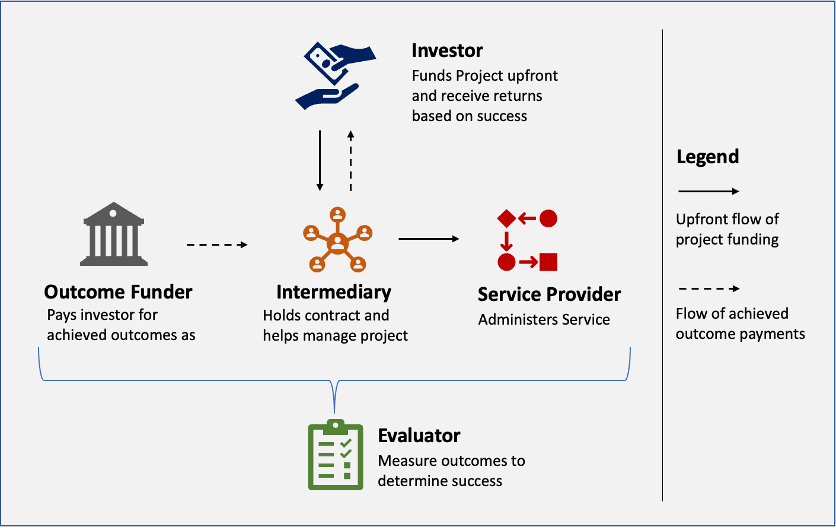

Blended finance (BF) has been established in India for over a decade, with several successful transactions. Yet, the ecosystem remains relatively nascent and is limited to a few philanthropies, development finance institutions, and investors. Dalberg, a global social impact advisory, has been at the forefront of moving the needle on these efforts across sectors such as education, climate, skilling and healthcare in India. The firm has advised leading Indian and global investors on impact investment strategies, developed blended finance funds for large organisations, and participated in outcome bond programmes such as the Quality Education India- Development Impact Bond (QEI-DIB) and Skill Impact Bond (SIB).

Tushar Thakkar, Associate Partner at Dalberg Advisors, has led several of these initiatives. Given that these instruments are fairly new and quite complex, they are perceived to be risky and expensive by many funders who may be interested but are waiting on the sidelines, says Thakkar. In this interview, Thakkar breaks down the complexities of setting up and operating blended finance transactions, and shares a five-point framework to address these challenges.

Q1. In your experience with practitioners working to structure blended finance instruments, what are the challenges that hinder adoption and mainstreaming of these transactions?

The most pressing problems are the ones posed by the complexity of blended finance structures. They involve multiple stakeholders, each with different priorities, perspectives, and objectives. We have private actors and philanthropic actors, and they don’t always speak the same language. While the presence of different types of capital providers is the strength of blended finance structures, helping expand the capital pool and driving stronger incentivisation towards developmental goals, it is also a challenge. In India, specifically, regulations for philanthropic actors and the private sector have evolved separately, leaving limited room for these two different funding pools to come together, though this is now changing with new initiatives like the Social Stock Exchange. In addition, given how new blended finance instruments are, there is inadequate understanding among each actor of what drives success for the others.

What adds to the complexity is lack of standardisation and limited number of precedents to learn from. While the ecosystem is expanding, these instruments are still fairly ahead of the innovation curve, requiring more research and time, and therefore greater upfront investment. On average, structuring a blended finance instrument today takes 1.5-2 years. It tends to scare funders and other participants away.

Organisations face resource constraints, including the availability of team members with the requisite expertise and knowledge gaps as well as infrastructural constraints such as lack of data systems or payment systems. Precise data, for instance, determines how you price the metrics – so these details matter. This again ties to the problem of the lack of precedence.

Q2. What is an approach or framework you would suggest to address these challenges?

As more and more blended finance transactions are undertaken, longer term systemic solutions are being developed. With more transactions, there will be greater understanding of blended finance approaches, supported by evolving regulation. There is also an ongoing push towards reducing complexity and, consequently, upfront cost, which will happen as the sector matures. While we wait for this to happen, there are approaches that can be utilised by interested funders and implementing organisations in the interim.

During the setting up stage, effective sequencing and stage-gating can help manage investments and force key decisions at appropriate times. In the projects that we have worked on, we advise clients to identify key decision points early on and establish clear criteria for ‘go’, course correction, and ‘no-go’ decisions. If there is a hypothesis that a particular instrument will work for a particular sector, then working with consortium partners on a rapid feasibility study to confirm the hypothesis is better than jumping into 6-9-month detailed design project right off the bat. Aligning on these decisions and committing to them upfront is crucial, and there should be no hesitation in adjusting commitments based on findings. There is often a desire to continue, just because a lot of funds have been spent by different stakeholders. This is known as the sunk cost fallacy. Avoiding this trap entails making decisions based on whether they help meet objectives, and not on how much money has already been spent.

Early identification of instrument fit is key. There is substantial excitement around blended finance and we get lots of clients who want to structure these instruments. But there are multiple other instruments that may be a better fit. By leveraging the limited yet valuable public knowledge and forums available, it is possible to determine whether a particular intervention or impact area is suitable for utilising blended finance, and the type of blended finance, as opposed to grants. Proceeding without a sufficient basis for the chosen instrument often leads to added complexity at a later stage. We have seen instances where organisations have committed to an instrument without ensuring it meets the needs of the programme.

Bringing key stakeholders together at an early stage is crucial. This includes anchor funders or philanthropic actors, government partners, and implementation partners. Bringing them together early on allows organisations to tailor the design, define key parameters, and answer questions such as do we need risk mitigation; is this early-stage innovation; do we need more data. Conversations with them provide valuable feedback on which intervention types and designs resonate. Similarly, funders should ensure the presence of high-quality implementing partners that can deliver what they seek.

During the implementation stage, organisations must anchor efforts on strong contracts tied to core outcomes and associated actions such as targets, pricing, and metrics. Given that the development sector is data-scarce and highly uncertain, secure contracts help mitigate conflicts and delays related to operational concerns. However, it is advisable to maintain flexibility in other aspects, such as innovation and ecosystem change, unless they are explicitly part of the outcomes being funded.

Planning and codifying responses to ‘known unknowns’. For instance, if organisations believe the climate will have a strong impact on their sector, they must account for that. One of our outcome-based programmes – the Quality Education India Development Impact Bond – overlapped with the Covid-19 pandemic. This was a scenario where partners were able to arrive at solutions through highly collaborative action, but it did require a fair bit of effort. Thinking through and planning efforts to meet unprecedented challenges helps.

Q3. You stated that there is a need to identify key decision points early on. What are some aspects an organisation should be cognisant of to implement an actionable and sustainable investment strategy and limit course correction?

At a conceptual level, the way to sequence decision points is to think about what could lead to failure. What this means is answering questions such as: is this the right instrument for my organisation? Is there a funding market for these developmental objectives? If yes, is it deep enough? Is there a funder who shows substantial interest? Is the regulatory environment favourable of the structure? If the answer to any of these questions is no, that increases the risks of failure. These are the higher-order questions to answer first in the first few months.

Once you have resolved those and are comfortable with the instrument, you can think of the second-order questions. What donors care most about is the beneficiary profile, which includes details such as the concerned demographics and geographies. This must be defined sharply. Next, you get into the operations questions; these are decisions linked to pricing, partners you want to work with, quantum of funding, return expected, operating model, and mode of engagement. Once key members of the consortium are all on board, these questions are relatively easier to answer and low risk.

Q4. What are the criteria organisations could follow to match their investment approach and appetite to the right type of blended finance instrument or structure?

It is important to answer the question – why not a grant approach? Grant instruments have been around for a long time, so there is a good understanding of how they work. They are also a relatively low-cost instrument. So, the question ‘why not grants’ should be answered first. There could be many reasons – the quantum of capital may not enough, or risk-averse donors may fund only specific types of interventions. Organisations need to identify the problem that they are trying to solve for, compared to a simple grants-based model, and for which stakeholder. Barriers include high risk perception, cost of capital, shortage of capital, or lack of appropriate incentives. Determining which of these barriers need to be addressed will help in appropriately designing the instrument and financial structure.

Once you have the answer, it should be followed by the question – if not grants, then what? Blended finance instruments, in comparison, are complex. Organisations need strong reasons to move towards them, and decision-making comes under five buckets. One, determining the key characteristics of the intervention being funded and its required cash flow profile. This includes the kind of sector, the beneficiary profile, the type and quantum of funding. Two, understanding the stage of the intervention – early-stage, developing, or mature. This matters because early-stage interventions are risky and need different stages of capital than mature ones. Three, analysing the type of organisation that is asking for funds. Whether it is a for-profit or not-for-profit body determines how it can absorb the money. Finally, assessing the regulatory boundaries around which you are building the structure.

While transactions are currently largely based on private contracts between key stakeholders, emerging platforms such as the Social Stock Exchange are likely to become strong, viable alternatives for hosting blended finance transactions. These trends need to be observed and could potentially be important inputs into the design process.

Q5. You mentioned that aligning with the right implementation partner can help monitor target outcomes. Do you have any suggestions on how practitioners could design a monitoring and evaluation framework in advance and implement it with a mission-aligned partner to ensure better transparency and effective utilisation of funds?

Our experience with blended finance instruments in general, and outcome-based funding specifically, indicates the need to assess three things – culture, system, and scale. Implementing organisations, including the management and other stakeholders, need to be culturally aligned with the proposed outcomes. They must be open to tailoring and modifying the intervention approach as the transaction requires. We have seen organisations that don’t have this flexibility struggle with the partnership. Next, availability of requisite systems should be ensured. Outcome instruments are tied to very specific metrics, and so there is a need for a strong internal MEL, data collection, and data reporting systems. Organisations that have these systems are better placed to enter such partnerships. Finally, the objective of most organisations is to start small and then scale. Organisations that have capacity to scale are ideal. This could mean those that are already operationally large or those that have the potential to grow within the boundary of the program. Organisations rarely get a perfect implementation partner right off the bat and they need flexibility to get there. Developing MEL frameworks early can help organisations figure out if they need to change culture and incentives, invest in particular systems, and take other crucial decisions.

Q6. An important aspect you highlighted was being mindful of ‘known unknowns’, which greatly helps new entrants in the blended finance space to design and execute these structures. In your experience, what need to be considered while designing a flexible structure?

At the ecosystem level, there are two factors to consider. One is the growing impact of climate events. We are already seeing the adverse effects of climate change and know they are likely to increase, with each sector being impacted differently. While instruments must ideally be designed to account for them, they can be difficult to predict, such as with the pandemic. The other factor is regulatory structure. While regulation can simplify and streamline certain things, it is still evolving. Blended finance structure must create a platform for stakeholders to come together and evaluate mid-stream whether there is an easier way to achieve an objective.

At the organisational level, it is important to plan for financial or organisational distress among key stakeholders, which may restrict their ability to participate in the structure in the future. Compared to the commercial space, for example, the development sector does not have robust structures to deal with financial distress or bankruptcy. In such a scenario, how do you meet outcomes?

At the program level, severe underperformance vis a vis impact targets could pose another significant challenge. There will always be risks associated with future achievement of target outcomes. Ideally, these risks should be captured as part of a financial structure tailored to meet worst-case scenario situations. Thorough contracts with provisions for conflict resolution at the program level and flexible governance structure at the consortium level are the imperative tools to tackle these challenges.