Introduction

Powering Livelihoods is a multi-donor supported initiative implemented jointly by CEEW-Villgro. The initiative aims to boost India’s rural economy by scaling up the penetration of clean energy-powered appliances for livelihoods. Over the last three years, the program with its financial and technical assistance has supported 17 innovators with field-tested technologies to undertake large-scale commercial deployments.

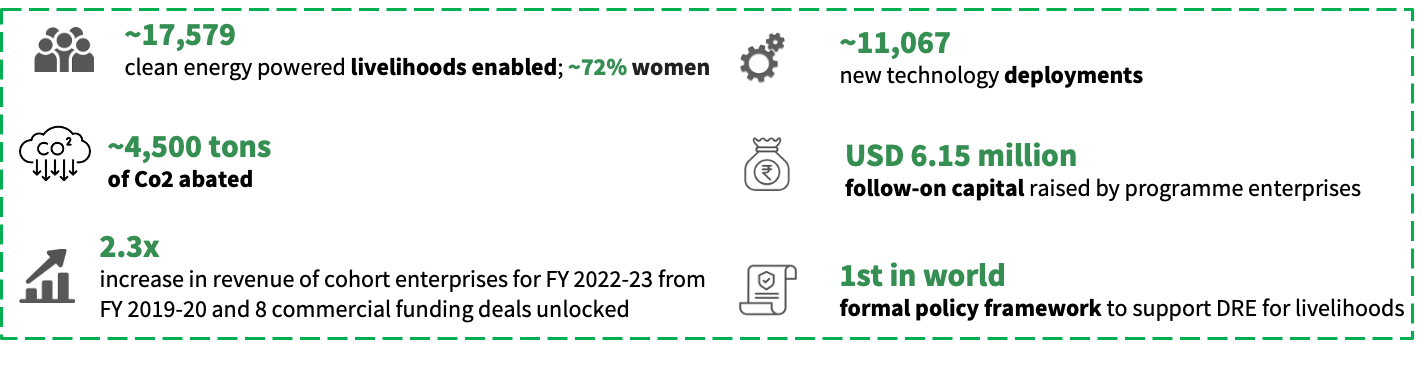

The program’s impact so far

Leveraging Partnerships to unlock commercial capital for scaling solutions

To support the scaling of Decentralized Renewable Energy (DRE) based solutions, the initiative aimed at increasing access to finance to the end-users of these solutions. To increase access to finance the program designed risk mitigation interventions by blending philanthropic capital to attract commercial capital.

The Key FI partners in this program and insights from their intervention:

With this brief introduction to the Powering Livelihood program, we now move to an Exclusive Interview with Srinivas Ramanujam, CEO of Villgro, Unraveling On-Ground Impact, The Role of Partnerships, Blended Finance Interventions and Key Program Insights.

- Villgro’s initiative – The Powering Livelihoods program is aimed at empowering India’s rural economy by scaling up the penetration of clean energy powered appliances. Could you shed some light on how this initiative came about and what is Villgro and CEEW’s role in the program?

The program was conceived in 2020, on the back of a study done by CEEW which showed that unreliable electricity is a challenge for more than 40 Lakhs small businesses, presenting a USD 50 Billion market opportunity for Decentralized Renewable Energy (DRE) based solutions to step into this gap. Powering Livelihoods aimed to work at two facets of the problem – identifying and scaling up DRE Livelihoods innovators (Villgro’s forte) and in parallel strengthening the financing and policy framework to support this (CEEW’s strength area). Over 3 years, the program worked with 17 innovators, carefully selected for their mature products and scalable business models. It also established strong partnerships with rural distribution companies, state rural livelihood missions and financing companies that could give loans to customers of the innovations. - Through this program, Villgro has brought together both commercial and concessional capital providers for extending financial assistance to social enterprises, in scaling up their solutions to the last mile. Who were the financial partners who participated in this initiative and what were the financial structures that emerged from these partnerships?

It would be very helpful for our readers to understand the strategy behind mapping the blended finance structures to the relevant enterprises.

In the DRE sector, end user financing is very critical. Farmers or textile workers need loans to procure DRE products that help them earn better livelihoods. With end user financing in place, DRE enterprises can sell more products, scale up their operations, and in turn become eligible for financing themselves. In other words, end user financing is the precursor of enterprise financing.

In Powering Livelihoods, we constituted a financiers’ committee that brought together representatives from venture funds, NBFCs and philanthropies. Using the combined expertise of the committee members, we designed some interventions that would ease the flow of end user financing. These interventions used philanthropic capital in the following ways:

First loss default guarantees (FLDG) : where a pool of money was placed as a guarantee against the loan given to end users. This increased the comfort factor of the lender in lending to new borrowers.

Interest subvention: Philanthropic capital was deployed to reduce the interest rates for first time borrowers, thus helping to remove certain mind blocks towards taking the loan.Buy-back pool: Here philanthropic capital was kept aside to support a buy back of non-performing assets and deploy them in new locations.

Enterprises like Devidayal Solar (DRE powered refrigerators), Raheja Solar (solar driers), New Leaf Dynamic (biomass powered cold rooms) and Hydrogreens (solar powered hydroponic fodder unit) benefited from these interventions. The pilots were supported by financiers like Samunnati, Ashv Finance and Sanghamitra.

- We understand the program has focussed on empowering those climate innovations which can create on-ground impact and also hold the potential to provide commercial returns to investors.

Through this initiative what were some of the solutions or business models within renewable energy that you came across that you believe hold potential for scale with the support of blended finance?

Through the program Villgro was able to pilot blended finance solutions that allows end-users with access to finance for products that enable livelihood for them. Typically rural end-users will not have collateral, credit history or understand impact linked finance instruments. For banks and NBFCs, providing financing to small holder farmers or rural end-users is not financially viable due to the poor credit-worthiness or the ticket size.One successful example of a business model that showed promise of being able to scale with a blended finance solution was a solar dryer in the portfolio. The solar dryer helps to increase the income of farmers and uplift them by reducing their post-harvest losses, by creating value added products from the produce which otherwise goes waste or sold at very low prices. The enterprise helps with marketing and distribution of products created by the end-users of the dryer, solving the issue of market connect for them and creating predictability in income.

Cold storage solutions, powered by renewable energy, were also successfully piloted with financing solutions. There is a shortage of an established cold chain network in India, especially in rural areas. With utility across the value chain from farmers, to distributors and small retailers DRE cold storage solutions are a large market and by enabling end-users to purchase these products we were able to see improvements in livelihoods and income.

- Financing the underserved segment has been perceived as high-risk by traditional financing.Were there specific financing challenges that got addressed through the blended finance structures, which would otherwise have been difficult to manage through conventional financing mechanisms?

The main challenges addressed were: from the lender’s viewpoint, the risk appetite and comfort factor while lending to NTC (new-to-credit) borrowers as well as the apprehension about product usage and backup plan in case of non-functional sites; from the borrowers perspective, mind block against high interest rates; and overall, giving thrust to innovative business models. - Any key takeaways from this Program that you’d like to share? Challenges across different aspects of the program (at each stage – design, structuring, partnerships, impact measurement) that could be addressed going forward?

Here are some of the key takeaways:

1). “Closed loop” business models are favoured by financiers. When an enterprise sells a product, but bundles this along with a market linkage offering, it becomes much easier to finance the scheme because there is an assured cash flow. e.g. Raheja solar sells driers but also assures buy back of the dried produce, thereby giving comfort to financiers that there are sufficient cash flows to service their loans2). Collection risk is a big factor for financiers to take the plunge and issue loans. This is more acute when the users are located in far flung areas. This can be addressed by the enterprise, or their go-to-market partner, entering into a BC (business correspondent) agreement with the financier and helping to service the loan

3). The recent RBI guideline around FLDG has created some confusion among lenders, and it will take some time for the dust to settle around this so that universally acceptable blended finance models can emerge again

- Going ahead, what would be the Program’s focus areas? Is Villgro looking to play an extended role beyond its current scope of work?

From the first phase of the program, our experience and insights have shown us that we need to actively enable ecosystem support — by enabling partnerships with financiers, GTM partners and state governments — beyond supporting enterprises to further mainstream DRE livelihoods. The emerging need is to be more hands-on than only being a catalyst. Several new partnerships and ideas have been initiated. They showed great promise and opened up new avenues to promote the use of DRE for Livelihoods. The next phase of the program aims to take forward these initiatives and scale them up to achieve greater impact.

While there will be a focus on building awareness and driving demand with our GTM partners, a key enabler for the next phase will be ensuring end-user finance solutions for the DRE products. We were successful in providing the solutions by using philanthropic money to provide first loss default guarantees to reduce the risk to the financers, as well as to reduce interest rates for first time borrowers to reduce friction from end users. We will continue to work with our existing partners and will be looking to enable relationships with new ones, with the goal that as we prove impact and understand the risk, we improve the terms such as guarantee requirements and interest rates. - In your opinion, how could Blended Finance structures such as these be mainstreamed and made sustainable? Are there any stakeholder groups, who should participate more in initiatives like these? How could this be facilitated?

Blended finance for end user financing holds great promise for impact. It enables the creation of green livelihoods and brings communities into the formal banking system. Even as digital platforms take centre stage, there is still the perception of collection risk from rural areas. This can be overcome only if there is a strong partnership between financiers and intermediaries like enterprises, go-to-market providers and/or NGOs who can bridge this gap.